Revenue.

Margin.

Valuation.

Three numbers your board reads. AI is rewriting all three in your industry.

This briefing tells you where revenue, margin, and valuation move in enterprise SaaS as AI rewrites the industry. Read it before your competitors decide what your next decade looks like.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

Enterprise SaaS built its defensibility on three pillars: integration depth that punished switching, accumulated customer-specific configuration, and a feature set that took competitors years to replicate. AI has collapsed the third pillar. AI-native entrants now reach feature parity in twelve to eighteen months. The integration moat is weakening as modern migration tooling makes switching cheaper every quarter.

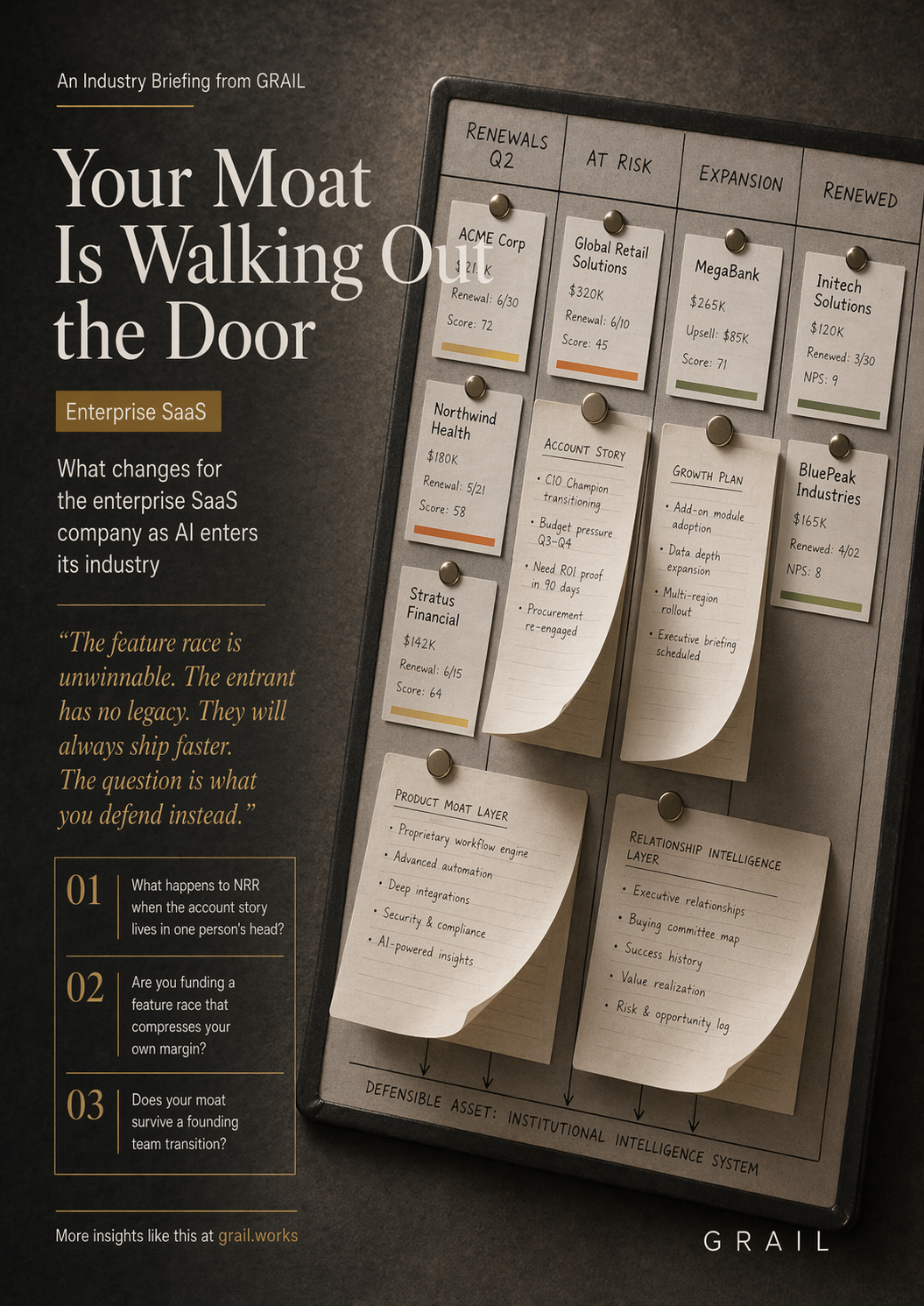

The real moat was never the product. It was the intelligence behind the product. And that intelligence sits in a handful of people's heads.

What remains is the accumulated intelligence itself: why the data model is structured this way, what the regulator actually enforces versus what they publish, which accounts are expanding and which are quietly disengaging. That intelligence exists in two places, both fragile. Customer intelligence lives in CSM heads, not in CRM. Product knowledge lives in three to five founding engineers. When either walks out, the company loses something that cannot be rebuilt from dashboards or documentation.

For the CEO of an enterprise SaaS company, this is not a people problem. It is a revenue problem, a profit problem, and a valuation problem simultaneously.

Revenue. Profit. Valuation.

Three lenses. Three answers the management team needs before the next board call.

Revenue

AI-native entrants now appear in every competitive review. They ship faster because they carry no legacy architecture. Your new-logo win rate is already shifting. Expansion ARR is compensating, but expansion depends on CSMs who understand the account deeply enough to spot the opportunity. When a senior CSM leaves, account health degrades within 90 days in ways dashboards do not show until the renewal is at risk.

Profit

Competing on feature velocity against entrants with no technical debt compresses margin from both sides. Their cost of delivery is lower. Your pricing power erodes as feature parity closes the gap. The pressure to hire more engineers to keep up accelerates the margin squeeze. The profit question is whether you are funding a feature race that cannot be won, or investing in intelligence infrastructure that compounds.

Valuation

The ARR multiple investors assign depends on how they price your moat. Personal intelligence held by a handful of people is a discount, because it introduces key-person risk at every level. Institutional intelligence encoded into workflow, data model, and customer infrastructure is a premium. The same ARR, at very different multiples, depending on one architectural choice the leadership team makes now.

What you'll get when you download

A 10-page report for enterprise SaaS CEOs, founders, and management teams. Designed to be read in one sitting before your next board call.

The strategic choice, side by side

The default path (add AI features, compete on velocity, defend NRR with account management) and the repositioning path (encode dual intelligence, build institutional infrastructure, reprice the moat), with the financial logic of each laid out in a comparison table.

The four levers that compound

Encode product knowledge before founders leave. Turn customer interactions into institutional intelligence. Use AI to accelerate roadmap without hiring into the margin. Reprice the equity story around institutional moat, not feature count.

Five questions for your next board call

Diagnostic questions the CEO should test the leadership team against before the board asks them. The questions where the room cannot agree are the ones worth a longer conversation.

Calibrated for each seat at the table.