Revenue.

Margin.

Valuation.

Three numbers your board reads. AI is rewriting all three in your industry.

This briefing tells you where revenue, margin, and valuation move in asset management as AI rewrites the industry. Read it before your competitors decide what your next decade looks like.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

Active investment management built its value proposition on a simple claim: our people see what others miss. That claim worked when the seeing was genuinely scarce. Market screening, factor analysis, data aggregation, peer benchmarking. AI has commoditized every piece of the quantitative seeing. The screening that took a team of three now runs in minutes.

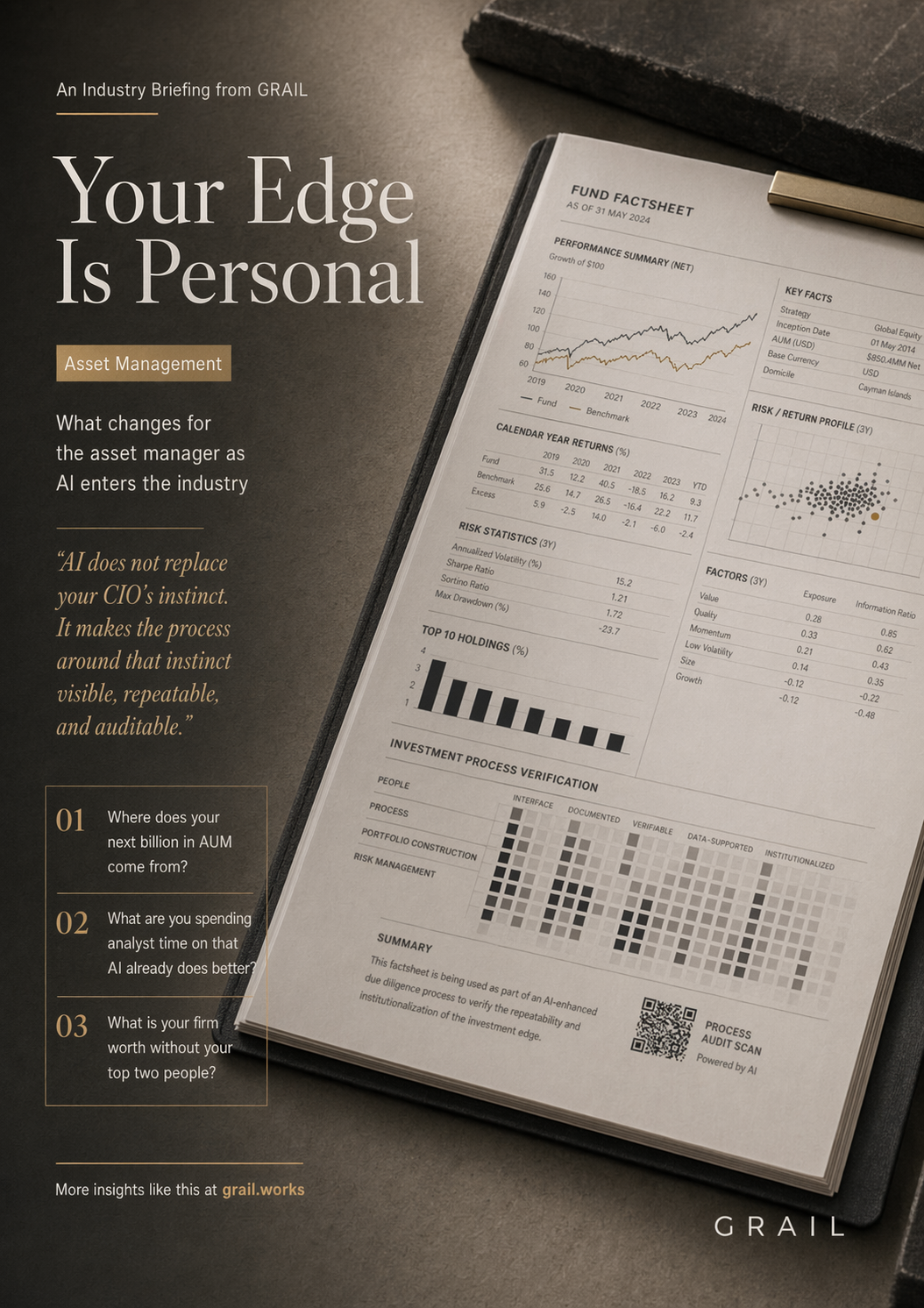

AI does not replace your CIO's instinct. It makes the process around that instinct visible, repeatable, and auditable. That is the difference between a fund and a franchise.

What remains defensible is the investment thesis itself: the qualitative judgment about why a sector, a management team, or a structural trend will play out differently than consensus expects. That judgment lives in two or three heads. It is not documented in a form that demonstrates institutional repeatability. LPs know this. AI-powered due diligence platforms are giving allocators the tools to test the answer.

For the CEO or CIO of a mid-market asset management firm, this is not a technology question. It is a revenue question, a profit question, and a valuation question.

Revenue. Profit. Valuation.

Three lenses. Three answers the leadership team needs before the next LP meeting.

Revenue

Capital allocation decisions are shifting toward funds that demonstrate systematic investment process. Every fundraise, every LP review, every mandate competition now includes questions about process repeatability. The fund that shows how judgment gets applied consistently wins allocations over the fund that says "trust our team."

Profit

Every hour your investment team spends on data assembly, market screening, and report generation is an hour not spent on the qualitative judgment that differentiates. Competing on quantitative speed against firms with better AI infrastructure compresses margins without producing differentiation. The profit question is whether your cost structure reflects where your actual edge lives.

Valuation

The equity multiple on a management company depends on how a buyer prices the durability of the AUM. Key-person risk is a discount. Institutional process that survives leadership transitions is a premium. The same AUM, the same fee income, at very different multiples depending on one question: is the edge personal or institutional?

What you'll get when you download

A 10-page report for asset management CEOs and CIOs. Designed to be read in one sitting before your next LP meeting.

The strategic choice, side by side

The default path (automate the quant layer, compete on data processing speed, keep the edge personal) and the repositioning path (make the judgment visible, institutionalize the process, turn documentation into a fundraising asset), with the financial logic of each.

The four levers that compound

Document the investment process in institutional form. Build LP intelligence infrastructure. Free analyst time for judgment, not assembly. Turn process documentation into a fundraising asset. Each lever available now. Together, they convert a fund into a franchise.

Five questions for your next LP meeting

Diagnostic questions the CEO or CIO should test the leadership team against before the next allocator conversation. The questions where the room cannot agree are the ones worth a longer conversation.

Calibrated for each seat at the table.