Revenue.

Margin.

Valuation.

Three numbers your board reads. AI is rewriting all three in your industry.

This briefing tells you where revenue, margin, and valuation move in B2B SaaS and tech as AI rewrites the industry. Read it before your competitors decide what your next decade looks like.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

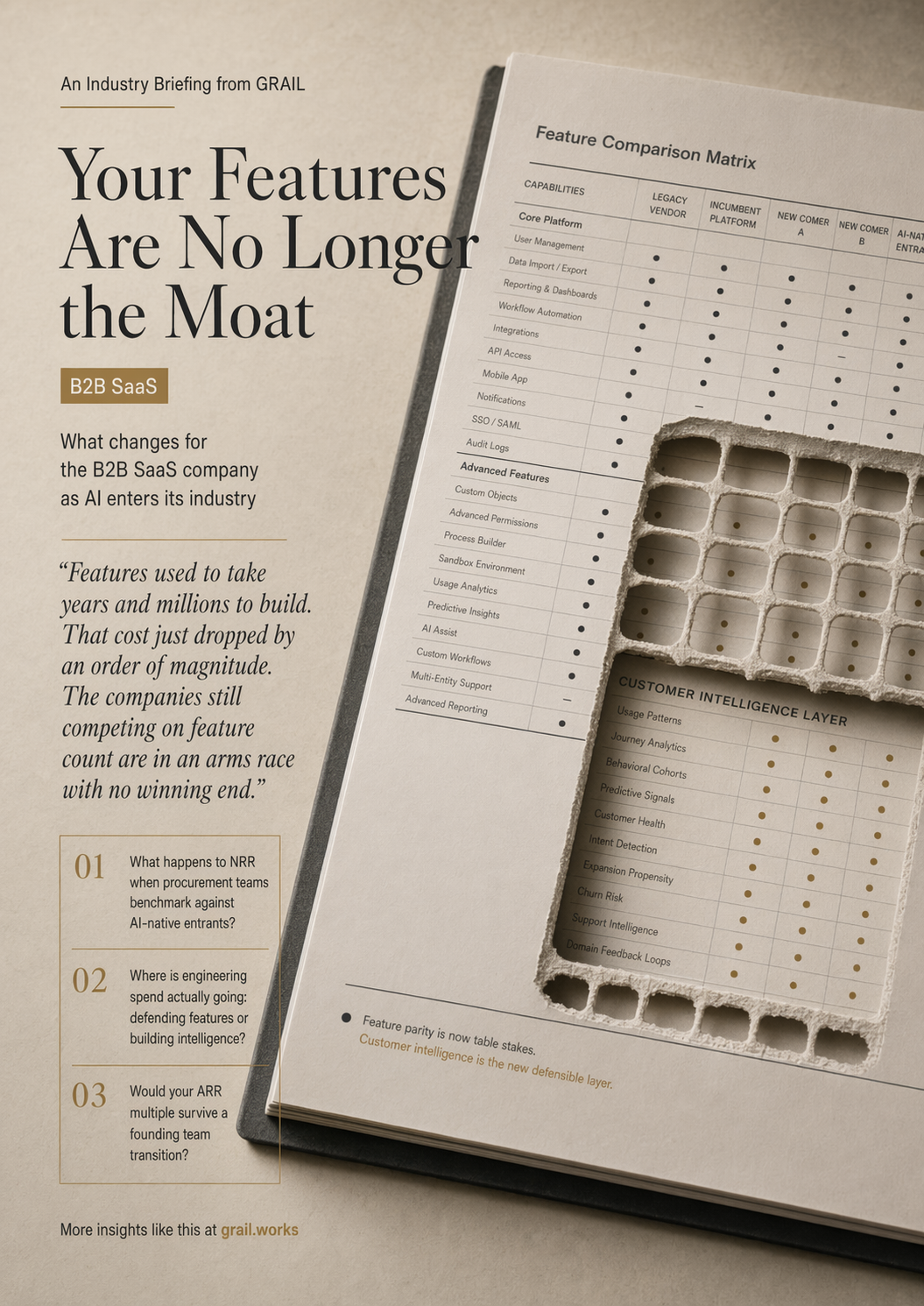

B2B SaaS built its defensibility on three pillars: workflow specificity that took years to encode, switching costs anchored in deep integrations, and data network effects that compounded with each customer. AI has collapsed the first pillar. The second is eroding as AI-native entrants invest in migration tooling that used to be uneconomical. The third remains, but only for the companies that have systematically captured what they know about their customers.

Features used to be the moat because they took years and millions to build. That cost just collapsed. The question is what you are actually defending.

What cannot be replicated by a well-funded entrant with a good foundation model: the accumulated understanding of why your customers bought, how they actually use the product, what their renewal risks look like six months before the data shows it, and what they need but have never articulated. That intelligence is the real defensible asset. It is also, in most mid-market SaaS companies, trapped in the heads of individual account executives and customer success managers. When those people leave, the intelligence walks out with them.

For the CEO of a B2B SaaS company, this is not a product roadmap question. It is a revenue question, a profit question, and a valuation question.

Revenue. Profit. Valuation.

Three lenses. Three answers the management team needs before the next board call.

Revenue

AI-native entrants reach feature parity in twelve to eighteen months. Every competitive deal, they are in the room with a modern architecture and lower price point. Your NRR is compressing. Procurement teams that never benchmarked during the growth years are running competitive reviews. The companies that demonstrate institutional customer knowledge depth outperform in those reviews. The ones relying on feature lists do not.

Profit

Competing on feature velocity against entrants with no legacy architecture compresses margins from both sides. Their cost of delivery is lower. Your pricing power erodes as the feature gap narrows. Professional services margins improve only when AI augments the delivery team. The profit question is whether you are spending engineering budget defending features or building intelligence infrastructure that compounds.

Valuation

The ARR multiple investors pay depends on how they price the moat. Customer intelligence trapped in individual heads is a discount. The same ARR with institutional customer intelligence encoded into product, workflow, and data infrastructure commands a premium. Investors are already adjusting: they ask about AI-native competitive exposure and knowledge dependency risk in every diligence process.

What you'll get when you download

A 10-page report for B2B SaaS CEOs and founders. Designed to be read in one sitting before your next board call.

The strategic choice, side by side

The default path (compete on features, add AI badges, ship faster) and the repositioning path (encode customer intelligence, compound domain depth, reprice the moat), with the financial logic of each. Where NRR holds and where it erodes.

The four levers that compound

Encode customer intelligence institutionally before key people leave. Turn every customer interaction into domain training data. Use AI to deepen vertical specialization faster than entrants can replicate. Restructure professional services around AI-augmented delivery.

Five questions for your next board call

Diagnostic questions the CEO should test the leadership team against before the board asks them. The questions where the room cannot agree are the ones worth a longer conversation.

Calibrated for each seat at the table.