Revenue.

Margin.

Valuation.

Three numbers your board reads. AI is rewriting all three in your industry.

This briefing tells you where revenue, margin, and valuation move in insurance as AI rewrites the industry. Read it before your competitors decide what your next decade looks like.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

Mid-market insurance built its competitive position on two assets: specialist underwriting judgment and long-standing broker relationships. AI is compressing both. Algorithmic pricing models commoditize the quantitative layer. AI-native MGAs are binding risk at half the turnaround time with structurally lower cost bases. Broker consolidation is eroding the informal advantages that came from decades of relationship trust.

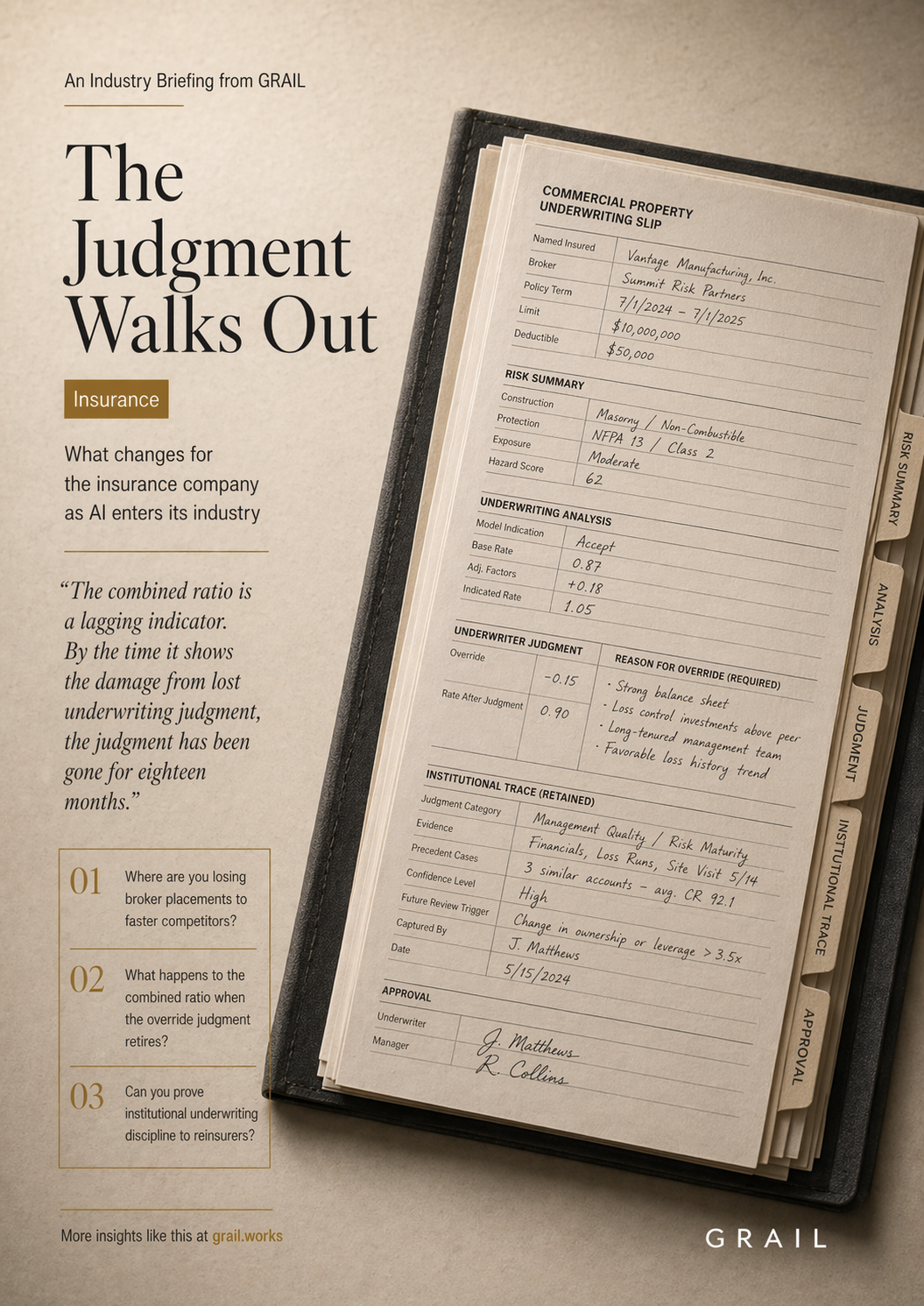

The combined ratio is a lagging indicator. By the time it shows the damage from lost underwriting judgment, the judgment has been gone for eighteen months.

What remains defensible is the override layer. The senior underwriter who looks at a model-approved risk and says no because they remember what happened to a similar book in 2008. Or who looks at a model-rejected risk and says yes because they understand a dimension the data cannot capture. That judgment is the remaining competitive asset. It is also entirely tacit, held by people approaching retirement, and invisible to every system in the organization.

For the insurance CEO, this is not an operations question. It is a revenue question, a profit question, and a valuation question.

Revenue. Profit. Valuation.

Three lenses. Three answers the management team needs before the next reinsurance renewal.

Revenue

AI-native MGAs quote in hours, not days. Brokers are consolidating and their loyalty follows speed and pricing. Every placement you lose to a faster competitor is revenue that does not come back. The broker does not call twice. The question is whether the underwriting quality that justifies a slower turnaround is visible to the broker or invisible.

Profit

The underwriters who override the model correctly are the ones keeping the combined ratio healthy. Their judgment is entirely tacit. When they retire, risk selection quality degrades invisibly for twelve to eighteen months. By then, the book is already damaged. The profit question is whether the organization can sustain underwriting quality without the people who currently provide it.

Valuation

Reinsurance capacity and pricing terms are set by confidence in the carrier's underwriting quality. Personal expertise in a handful of heads is a risk factor reinsurers quietly discount. Institutional underwriting discipline encoded into systems and processes is a premium. Same book of business, very different economics, depending on one architectural choice.

What you'll get when you download

A 10-page report for mid-market insurance CEOs and management teams. Designed to be read in one sitting before your next reinsurance renewal.

The strategic choice, side by side

The default path (compete on quoting speed, automate claims, match AI-native turnaround) and the repositioning path (encode the underwriting judgment, compound override intelligence, demonstrate institutional discipline to reinsurers), with the financial logic of each.

The four levers that compound

Encode override judgment before underwriters retire. Turn every risk decision into compounding intelligence. Compress the quoting cycle without sacrificing judgment quality. Build the reinsurance story around institutional discipline, not individual talent.

Five questions for your next leadership meeting

Diagnostic questions the CEO should test the management team against before the next reinsurance renewal. The questions where the room cannot agree are the ones worth a longer conversation.

Calibrated for each seat at the table.