Revenue.

Margin.

Valuation.

Three numbers your board reads. AI is rewriting all three in your industry.

This briefing tells you where revenue, margin, and valuation move in private equity and venture capital as AI rewrites the industry. Read it before your competitors decide what your next decade looks like.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

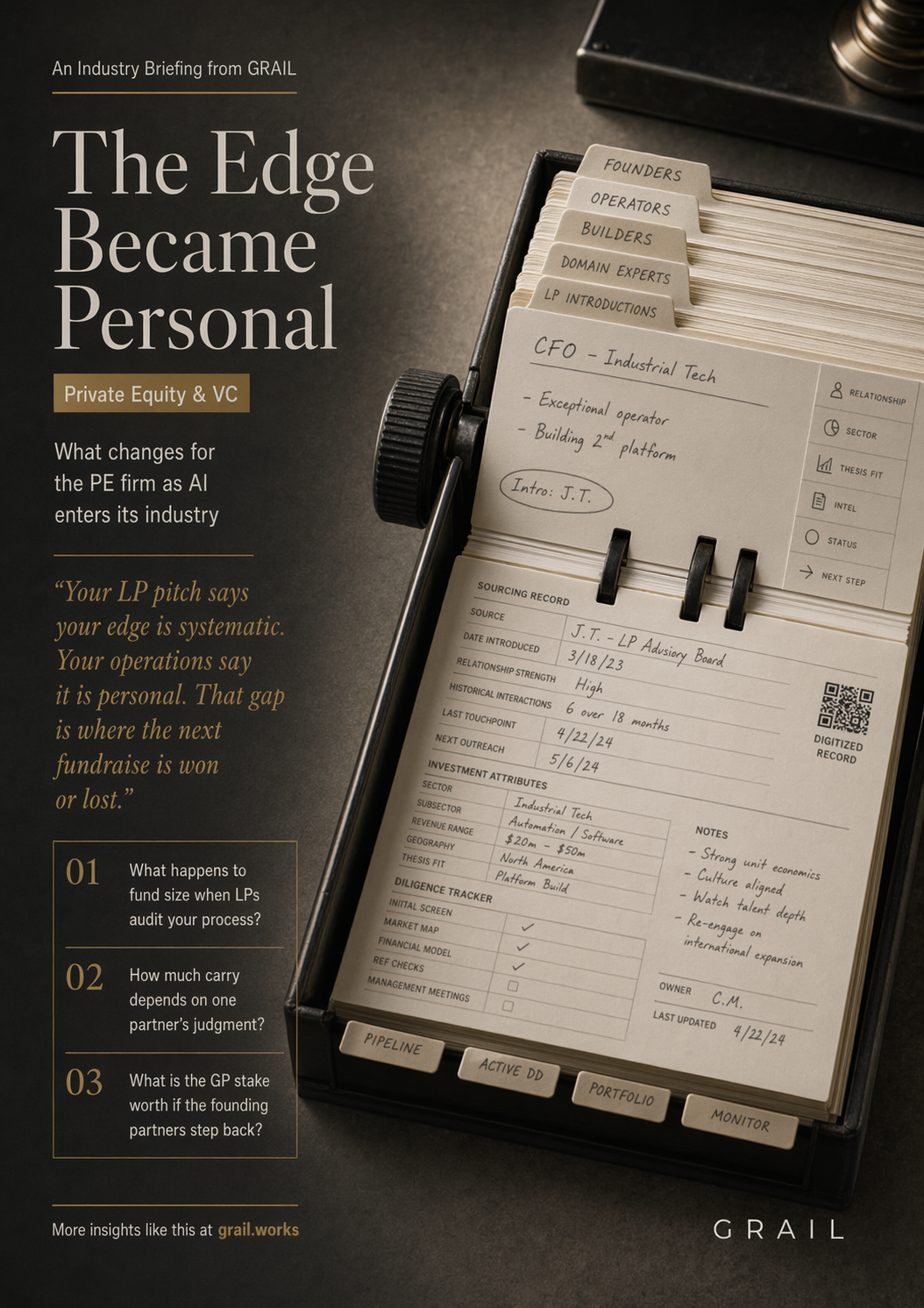

Mid-market private equity built its competitive position on three assets: proprietary deal flow through personal relationships, pattern recognition accumulated across investment cycles, and value creation playbooks refined through operational experience. All three are personal. They live in the heads of a handful of senior partners. When those people leave, the assets leave with them.

Your LP pitch says your edge is systematic. Your operations say it is personal. That gap is where the next fundraise is won or lost.

LPs are noticing. Sophisticated allocators increasingly ask what is proprietary about your sourcing, what is systematic about your diligence, and what is repeatable about your value creation. The GP who answers with references to track record and team experience is losing ground to the one who demonstrates documented, AI-augmented process that survives personnel transitions.

For the managing partner, this is not a technology question. It is a revenue question, a profit question, and a valuation question.

Revenue. Profit. Valuation.

Three lenses. Three answers the GP team needs before the next fundraise.

Revenue

Management fees are a function of committed capital. Committed capital is a function of LP conviction. LP conviction increasingly depends on whether your sourcing, diligence, and value creation are demonstrably systematic or visibly personal. The firm whose process survives scrutiny raises a larger fund. The firm whose process depends on three partners raises a smaller one.

Profit

Carried interest compounds when value creation is consistent across the portfolio, not concentrated in the deals one partner touches. Systematic diligence catches risks earlier. Systematic portfolio monitoring intervenes faster. Partner-dependent carry is a concentration risk LPs are learning to price.

Valuation

The GP stake is an asset. Its value depends on whether the firm can sustain returns through a generational transition. Personal edge in three heads is a discount. Institutional edge encoded into sourcing infrastructure, diligence process, and value creation methodology is a premium. Same fund, same track record, very different GP valuations.

What you'll get when you download

A 10-page report for mid-market PE and VC partners. Designed to be read in one sitting before the next fundraising conversation.

The strategic choice, side by side

The default path (AI as back-office tool, deal flow stays personal, LP narrative stays a story) and the repositioning path (AI as institutional edge, deal flow becomes infrastructure, LP narrative becomes evidence), with the financial logic of each.

The four levers that compound

Systematize deal sourcing before the next raise. Document value creation in auditable form. Build AI-augmented diligence that outperforms individual judgment. Make the systematic edge visible in LP materials.

Five questions for your partners' meeting

Diagnostic questions the GP team should test against each other before the next LP conversation. The questions where the room cannot agree are the ones worth a longer conversation.

Calibrated for each seat at the table.