Margin.

Pace.

Position.

The whole GTM playbook is being rewritten in real time, across every commercial team at once.

This briefing tells you how the GTM playbook gets rewritten in vertical software as AI compresses every commercial team. Read it before your competitors hit their first AI-native quarter.

The 10-page briefing. Worth 20 minutes.

One email. One PDF. Worth twenty minutes of your week.

We send it once. Work emails only.

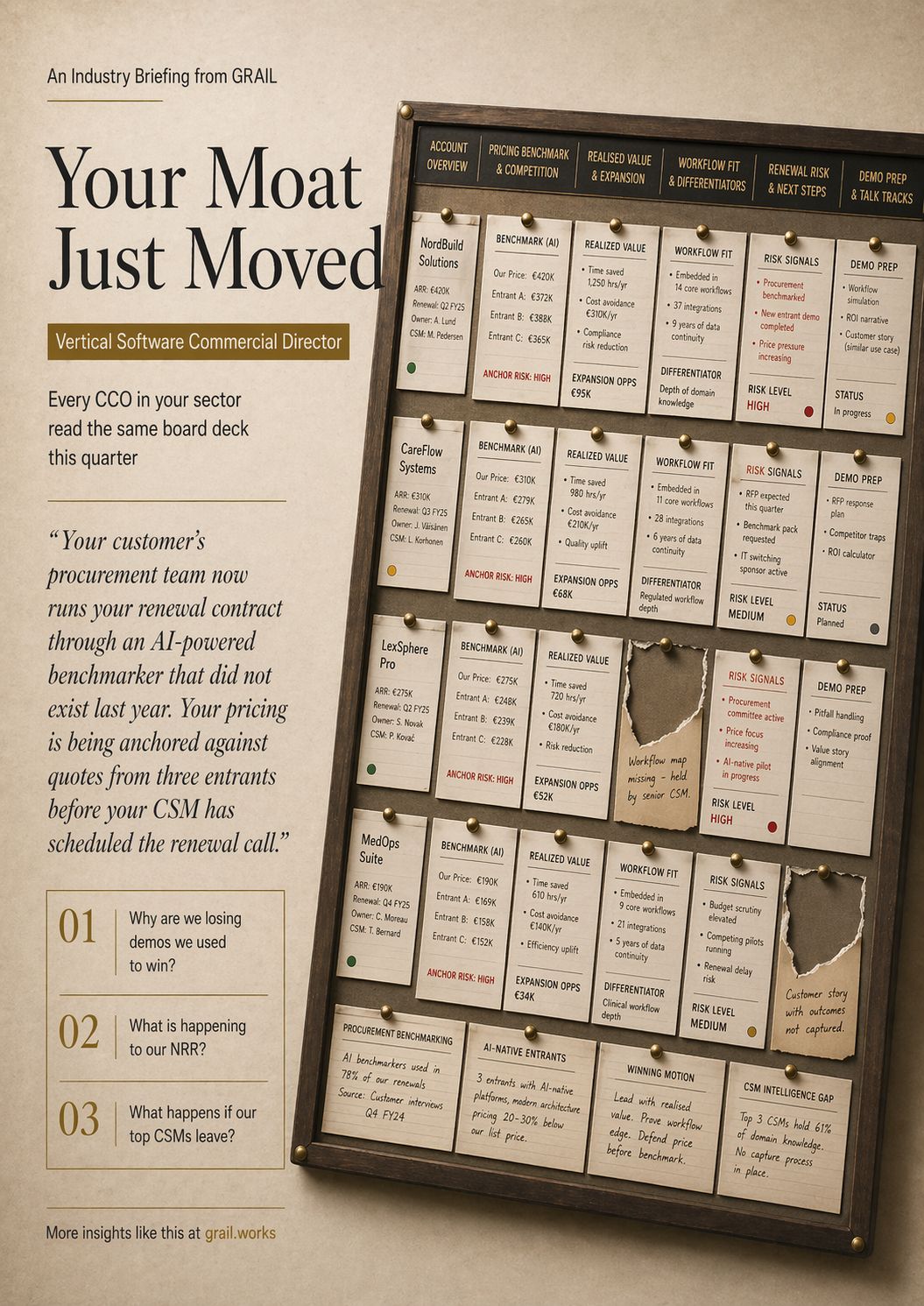

Every chief commercial officer at a vertical software company in Europe had the same week. The AI-native entrant in your vertical raised a Series B. They announced a customer logo you recognise. Your VP Customer Success came back from the user conference where three customers asked when your platform would ship the feature the entrant demoed in March. Your best account manager was approached twice this quarter.

You have done this job for a decade. The pattern used to be clean. Build a better product for the vertical than the horizontal platforms could. Hire great account people. Renew 95% of the book. The moat was five years of integrations, regulatory nuance, and workflow embeddedness. You had time.

The technical barrier collapsed. Your CEO and your board are asking what your moat actually is now. The honest answer is not your code. It is what your customer success team, your senior account people, and your implementation consultants know about how your customers actually work. That knowledge is the moat.

The entrant can out-ship you on features. They cannot out-know your customers. Your commercial team already has the knowledge.

Your CEO is already asking you about this. The briefing below is what you want in your hand before that conversation.

Pipeline. Retention. The moat nobody has measured.

Three questions every chief commercial officer in vertical software is being asked by their board. One year ago they were three separate conversations. They are one now.

Why are we losing demos we used to win?

The late-stage bake-off closed with the entrant you did not expect to see. They priced aggressively. They arrived better prepared. Your reps are not worse. The preparation race is being lost before the demo is booked, and the entrant's price anchor is in the procurement evaluation before your rep introduces themselves.

What is happening to our NRR?

NRR is the number your board actually watches. Every point you hold compounds. Every point you lose multiplies. Customer procurement benchmarking is compressing renewal pricing 3 to 8 percent industry-wide. Your expansion motion relies on knowledge that lives in three senior CSMs.

What happens if our top CSMs leave?

Your three best customer success managers, your senior implementation consultants, and your two long-tenure account managers carry the actual moat. Ten years of workflow reality lives in their call notes and their heads. Two of them were approached by the entrant this quarter.

What you get when you download

An 11-page report for chief commercial officers at mid-market European vertical software companies. Designed to be read in one sitting before your next leadership team meeting.

Your industry, your function, and why they are one problem

What is happening to vertical software as a sector. What is happening on your new-logo pipeline, in your customer success book, in your product marketing team right now. And the intersection most CCOs have not named yet. Plain language you can use in the boardroom.

Four moves across new logo, customer success, product marketing, and rev ops

How to get your reps into the demo with what your CSMs already know. How to capture what your CSMs know before they leave. How to stop selling features and sell your ten-year depth. How to rebuild the renewal motion around customer intelligence.

Five questions for your next leadership team meeting

Where your lost demos actually went. Where renewal pricing is really compressing. Your top CSM knowledge-transfer plan. Where your product marketing spends its week. And which of the four moves moves NRR the most in the next twelve months.

Calibrated for each seat at the table.